Your bankroll is the operating system that makes every other part of your betting strategy work. Without proper management, even a genuine edge will eventually be wiped out by a losing streak that was always statistically inevitable. This guide covers how to set up a bankroll, which staking plans work and why, how to survive variance, and the rules that separate disciplined bettors from those who go broke.

Table of Contents

- A bankroll is a dedicated pool of money set aside exclusively for betting, completely separate from everyday finances.

- The standard professional range for stake sizing is 1% to 3% of total bankroll per bet. Anything above 5% is considered aggressive and increases the risk of ruin significantly.

- Flat staking (same amount per bet) is the most reliable approach for bettors who are still building a track record.

- The Kelly Criterion calculates the mathematically optimal stake based on your edge and the odds, but should be applied at a fraction (25-50%) of the full output in practice.

- Chasing losses by increasing stake size is the single most common way bettors destroy their bankroll.

- Tracking every bet is not optional. Without records, you cannot measure your edge, identify weak markets, or make informed adjustments.

What a Bankroll Actually Is

A bankroll is not the money sitting in your bookmaker account. It is a deliberately ring-fenced pool of capital set aside for betting, funded only from money you can afford to lose entirely without affecting your financial situation.

The distinction matters practically: mixing betting funds with personal finances creates emotional pressure that degrades decision-making. When a losing run feels like it is affecting your rent or savings, the temptation to chase losses or increase stakes to recover becomes almost irresistible. Keeping the bankroll separate removes that pressure and allows you to make decisions based on logic rather than anxiety.

The size of your starting bankroll is less important than the discipline applied to it. A £200 bankroll managed correctly will outlast a £2,000 bankroll managed carelessly.

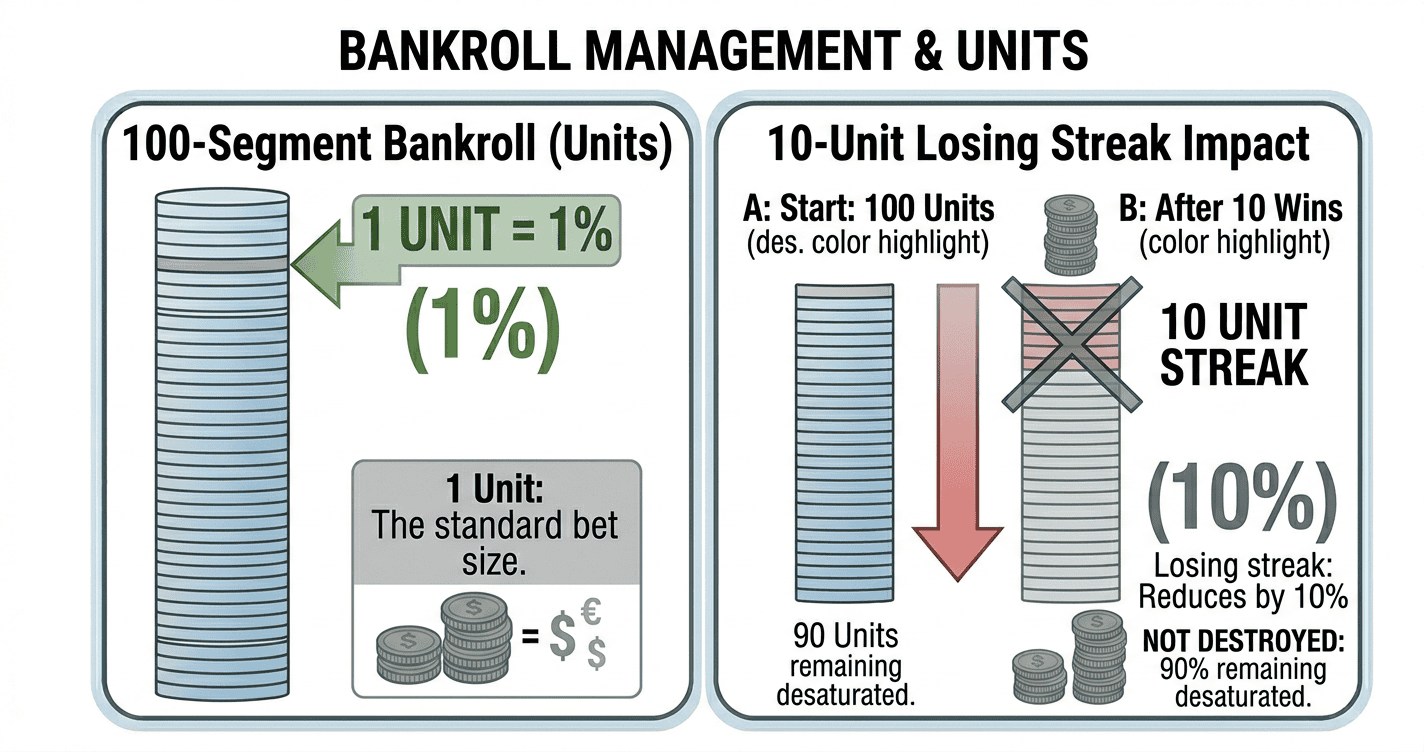

Units: The Universal Language of Staking

Professional bettors do not think in pounds or dollars per bet. They think in units, where one unit equals a fixed percentage of the total bankroll. This allows stakes to scale proportionally as the bankroll grows or shrinks, and makes it possible to compare performance meaningfully over time regardless of the nominal amounts involved.

The standard unit size recommendation:

| Experience Level | Unit Size (% of Bankroll) | Notes |

|---|---|---|

| Beginner | 1% | Prioritises survival over growth; maximises sample size |

| Intermediate | 1-2% | Appropriate once 200+ bets have been tracked |

| Experienced | 2-3% | Justified only with a verified edge over a large sample |

| Aggressive | 3-5% | High variance; only for bettors with strong, proven models |

| Reckless | Above 5% | Mathematically likely to result in ruin over time |

A common professional baseline is a 100-unit bankroll, where 1 unit equals 1% of the total. This gives 100 bets before the bankroll is exhausted even if every single one loses, which provides enough runway for variance to average out and genuine edge to show.

Staking Plans: Which One to Use

A staking plan is the ruleset that determines how much you bet on each selection. The right plan depends on your experience level, the accuracy of your probability estimates, and your tolerance for variance.

Flat Staking

Flat staking means betting the same unit size on every bet regardless of confidence level, odds, or perceived edge. It is the simplest and most reliable plan for most bettors, particularly those still in the early stages of building a track record.

The main advantage is that it removes the temptation to vary stakes based on emotional conviction. It also makes ROI straightforward to calculate and makes performance data easy to interpret.

Percentage of Bankroll Staking

Rather than a fixed nominal unit, the stake is recalculated each time as a percentage of the current bankroll balance. If the bankroll grows, stakes grow proportionally. If the bankroll shrinks, stakes shrink automatically.

Example with a 2% stake:

| Bankroll | Stake (2%) |

|---|---|

| £1,000 | £20.00 |

| £1,100 (after growth) | £22.00 |

| £900 (after drawdown) | £18.00 |

This approach means you can never go broke in theory (stakes always shrink before the bankroll reaches zero), but it also means recovery from a drawdown takes longer because stakes are proportionally smaller.

Kelly Criterion Staking

The Kelly Criterion is a mathematical formula that calculates the theoretically optimal stake size based on your edge and the odds on offer. It was first published by physicist J.L. Kelly Jr. in the Bell System Technical Journal in 1956, originally as a solution to information transmission problems. Mathematician Edward Thorp later applied it to blackjack and sports betting, documenting the method in his paper The Kelly Criterion in Blackjack, Sports Betting, and the Stock Market, which remains one of the most cited practical treatments of the formula. It maximises the long-term growth rate of the bankroll when applied correctly.

Or in a more usable form:

Where:

- b = decimal odds minus 1 (net odds)

- p = your estimated probability of winning

- q = probability of losing (1 minus p)

Example: you estimate a 55% true probability on a bet priced at 2.10 decimal.

- b = 2.10 – 1 = 1.10

- p = 0.55

- q = 0.45

- Kelly % = ((1.10 x 0.55) – 0.45) / 1.10 = (0.605 – 0.45) / 1.10 = 0.155 / 1.10 = 14.1%

Full Kelly recommends staking 14.1% of the bankroll on this bet. In practice, full Kelly is almost never used directly because it assumes your probability estimate is perfectly accurate, which it never is. Thorp himself noted that bettors tend to prefer staking somewhat less than the full Kelly fraction as a margin of safety against estimation error. Most professional bettors apply a fraction: quarter Kelly (3.5% in this example) or half Kelly (7%), which substantially reduces variance while preserving most of the growth advantage.

Staking Plans to Avoid

Several popular staking systems should be avoided in sports betting despite being widely discussed:

Martingale (doubling after losses). Doubling stake size after every losing bet to recover losses with a single win. The problem is that losing streaks long enough to make this unworkable are not rare events. A 10-game losing run (statistically expected at some point for anyone betting with 50% win rate) requires a stake 512 times the original on the 10th bet just to break even. This depletes bankrolls rapidly and hits bookmaker maximum stake limits before recovery is possible.

Fibonacci and other progressive systems. All systems based on varying stakes in response to results share the same fundamental flaw: they cannot change the underlying expected value of a bet. No staking system converts a negative-EV bet into a positive one. If the edge is not there in the selection process, no staking plan can manufacture it.

Risk of Ruin

Risk of ruin is the statistical probability that a given bankroll will be completely depleted before the edge has time to express itself over a large enough sample. It is determined primarily by two factors: stake size as a percentage of bankroll, and edge per bet.

The relationship is stark:

| Stake Size (% of Bankroll) | Edge Per Bet | Estimated Risk of Ruin |

|---|---|---|

| 1% | 3% | Very low |

| 2% | 3% | Low |

| 5% | 3% | Moderate |

| 10% | 3% | High |

| 1% | -2% (no edge) | Certain (eventually) |

The key insight is that stake size has more impact on ruin probability than edge size. A 3% edge with 10% stakes is more dangerous than a 1% edge with 1% stakes, because the variance from large bets can overwhelm the edge before it has time to compound.

The Monte Carlo simulation tool models thousands of possible bet sequences based on your edge, stake size, and bankroll to give a practical picture of how your specific parameters are likely to perform and what your realistic drawdown range looks like.

Surviving Losing Streaks

Losing streaks are not a sign that a strategy is broken. They are a mathematical certainty for anyone betting at odds above 1.00. The question is not whether you will experience losing runs, but whether your bankroll is structured to survive them.

Some reference points for context: a bettor with a genuine 55% win rate on even-money bets will still hit a run of 10 consecutive losses roughly once every 400 bets. At a 50% win rate, a 10-game losing streak is expected to occur roughly every 200 bets. Neither of these should cause a properly managed bankroll to drop more than 10-20% when staking at 1-2% per bet.

Rules for losing streaks:

- Never increase stake size to recover losses. This accelerates the rate of ruin rather than reversing it.

- Reduce unit size if the bankroll drops by 25% or more. Recalculate your unit as a percentage of the new, lower bankroll total.

- Audit your selections, not your staking. A prolonged losing streak is more often a signal to review market selection and probability estimation than to change the staking plan.

- Do not take a break from tracking. Stopping the record during a losing run creates a distorted performance picture and makes it impossible to learn from the period.

Tracking: The Non-Negotiable

No bankroll management system works without complete, honest bet tracking. The minimum fields to record for every bet are:

| Field | Why It Matters |

|---|---|

| Date | Identifies timing patterns and market conditions |

| Sport and market | Reveals which markets you have edge in and which you don’t |

| Odds taken | Essential for ROI calculation |

| Estimated probability | Lets you measure calibration over time |

| Stake (units) | Ties each bet to the bankroll management plan |

| Result | Calculates actual vs expected performance |

Calculating return on investment from your records:

A consistent positive ROI over 200+ bets is a strong signal of genuine edge. An ROI that deteriorates as sample size grows suggests the earlier results were variance rather than skill.

When to Adjust Stakes

Stake size should only be adjusted in response to meaningful, sustained changes in bankroll size, not in response to short-term results.

Scale up: after a verified 25-30% increase in bankroll, recalculate unit size upward proportionally. Do not scale up after a single winning session.

Scale down: immediately and automatically when the bankroll drops 20-25% from its starting point or its most recent high. This is not a failure, it is the system working correctly.

Never scale based on confidence. Varying stakes based on how certain you feel about a particular bet is one of the most common ways bettors distort their own data and introduce emotional decision-making into a process that should be mechanical.

Bettors who understand how bookmakers set their prices and build in their margin against you will recognise that the only durable edge comes from selection quality and consistency, not from betting more on the days you feel lucky.

Common Bankroll Mistakes

Treating the bankroll as a savings account. Withdrawing regularly for non-betting purposes or topping up after losses destroys the integrity of the system and makes performance measurement meaningless.

Overexposure through accumulators. Accumulator bets combine multiple selections whose individual probabilities multiply together. The bookmaker’s margin applies to each leg, meaning the overall implied probability of the accumulator is significantly worse than the true probability. A single-leg value bet staked at 2% is not the same risk profile as a 5-leg accumulator staked at 2%.

Ignoring sport-specific variance. Different sports have very different variance profiles. Football at odds around 2.00 has lower per-bet variance than tennis at odds of 6.00, which has lower variance than horse racing at 20.00. Bettors who operate across multiple sports and odds ranges should adjust their unit sizing accordingly, staking smaller units on higher-odds selections.

Mistaking a hot streak for a proven edge. A 10-bet winning run proves nothing statistically. Increasing stakes significantly on the basis of a short-term run is the same mistake as increasing them to recover a short-term losing run. The sample size required to confirm genuine edge is in the hundreds of bets.

FAQ

QHow much should a starting bankroll be?

QWhat is the safest staking plan for beginners?

QShould I use the Kelly Criterion?

QHow do I know if my edge is real?

QWhat should I do during a losing streak?

QDoes bankroll management work if I have no edge?