Most bettors lose not because they cannot find value, but because their own psychology works against them. The biases that drive poor betting decisions are hardwired patterns of human thinking, documented extensively in behavioural economics research, that distort probability judgements under conditions of risk and uncertainty.

Table of Contents

This guide covers the most damaging psychological traps in sports betting, where each one comes from, and the practical habits that reduce their influence over your decisions.

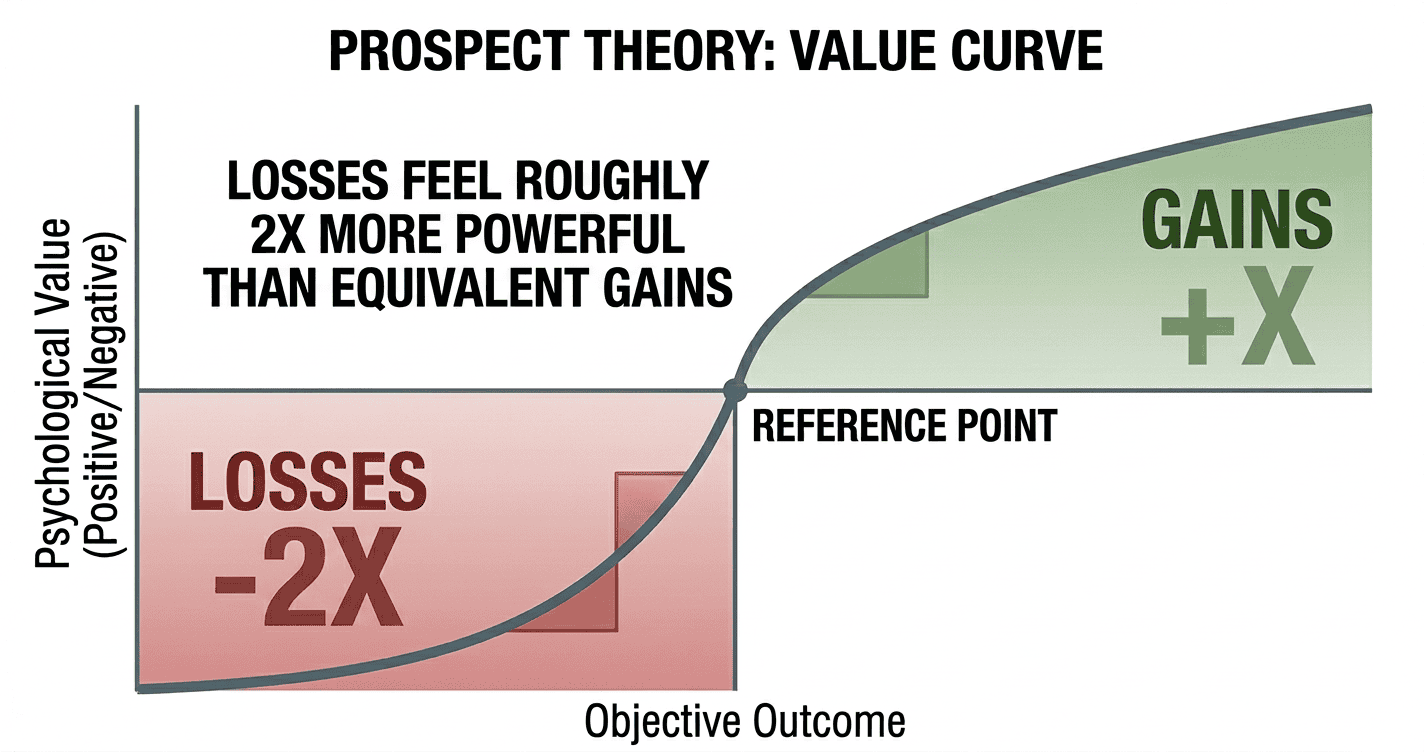

- Loss aversion, first described by Kahneman and Tversky in their 1979 prospect theory research, causes the pain of a loss to feel roughly twice as powerful as the pleasure of an equivalent win, driving most irrational betting behaviour.

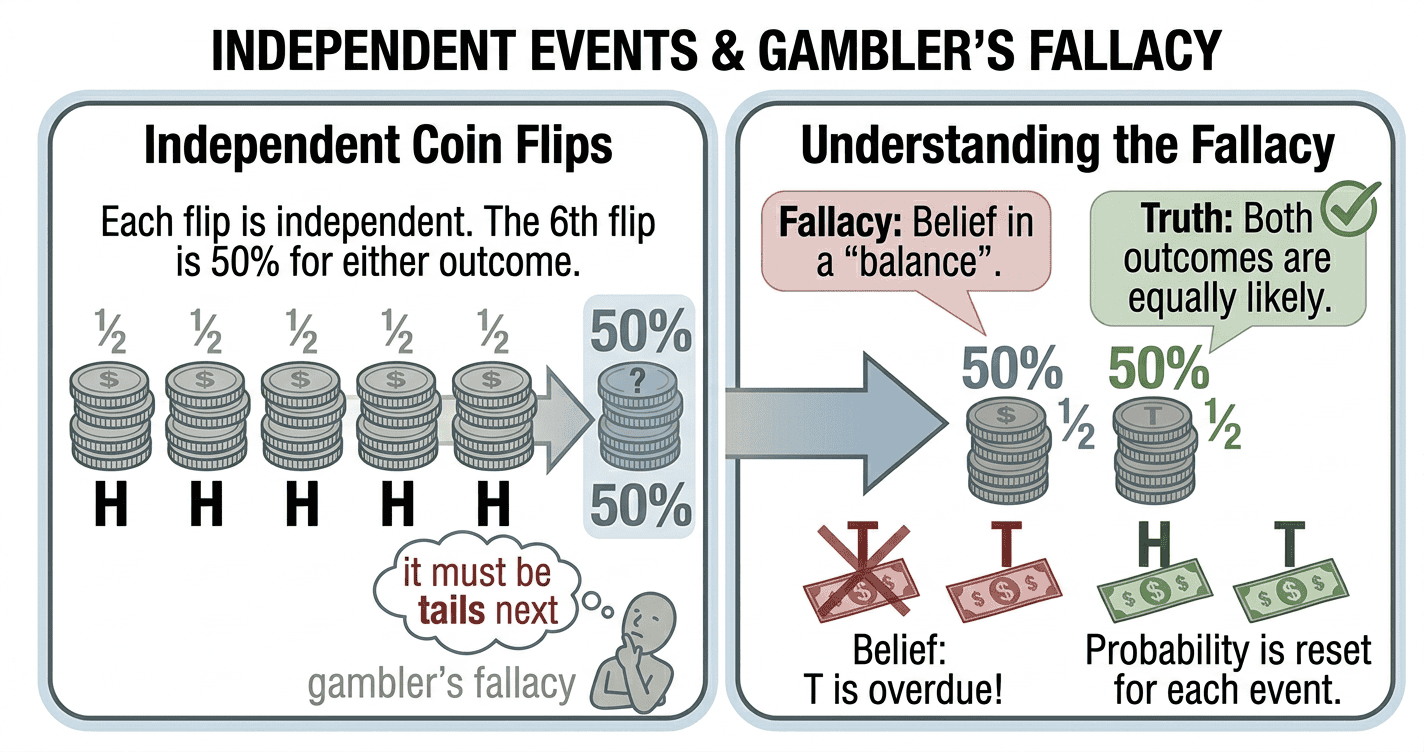

- The gambler’s fallacy is the mistaken belief that past independent outcomes affect the probability of future ones. It is one of the most common cognitive distortions in betting, present in casual and experienced bettors alike.

- Confirmation bias causes bettors to seek information that supports a position they have already taken and dismiss evidence that contradicts it, leading to systematically overconfident probability estimates.

- Tilt is the state of emotionally impaired decision-making following a loss or series of losses. It is the point at which most bankrolls are destroyed.

- The practical antidote to all of these biases is a pre-committed, process-based system: deciding criteria before looking at odds, recording every bet, and reviewing results on a schedule rather than reactively.

Biases at a Glance

| Bias | What It Does | The Fix |

|---|---|---|

| Loss aversion | Makes losses feel ~2x more painful than equivalent gains feel good | Pre-commit stake sizes; remove in-session decisions |

| Loss chasing | Drives stake increases after losing runs to “recover” deficits | Pre-set drawdown rules written before the session |

| Gambler’s fallacy | Creates false belief that past results affect independent future events | Treat every bet as statistically independent |

| Hot-hand fallacy | Creates false belief that a winning streak will continue | Anchor estimates to large sample data, not recent runs |

| Confirmation bias | Filters evidence to match a conclusion already reached | Actively list the strongest reasons NOT to place every bet |

| Recency bias | Overweights recent events when forming probability estimates | Use 10–20 match samples and stable metrics over recent results |

| Anchoring bias | Over-relies on the first price seen as a reference point | Form your own probability estimate before looking at odds |

| Overconfidence | Inflates perceived edge and win rate | Compulsory tracking against estimated probabilities |

| Sunk cost fallacy | Continues betting to recover a loss that is already gone | Evaluate each bet forward-only; session history is irrelevant |

| Tilt | Triggers emotionally-driven decisions that abandon process entirely | Recognise early warning signals; stop the session immediately |

Loss Aversion: Why Losses Hurt More Than Wins Feel Good

In 1979, psychologists Daniel Kahneman and Amos Tversky published their landmark prospect theory paper in Econometrica, introducing what is now one of the most replicated findings in behavioural economics: people do not weigh gains and losses symmetrically. The pain of losing a given amount of money is psychologically approximately twice as powerful as the pleasure of gaining the same amount.

In betting, this asymmetry has direct and damaging consequences. A bettor who has won £100 and then lost £100 is back to even, but the psychological experience is not neutral. The loss registers far more sharply than the win, creating pressure to act, to recover. That pressure is the origin of almost every self-destructive betting behaviour: increasing stake sizes after a losing run, placing unplanned bets to chase a deficit, and abandoning a disciplined staking plan in favour of one large bet designed to wipe out a session loss in a single outcome.

The practical counter to loss aversion is not willpower but structure. The bankroll management principles of ring-fencing betting funds and pre-committing to fixed unit sizes work precisely because they remove the moment-to-moment decision about how much to stake. When that decision is already made, there is nothing for loss aversion to manipulate.

Loss Chasing: The Most Expensive Behaviour in Betting

Loss chasing is loss aversion in action. It describes the pattern of increasing bet sizes, placing more bets than planned, or deviating from a selection strategy in direct response to a recent losing run, with the explicit goal of recovering what has been lost.

The logic feels intuitively reasonable: a deficit exists, larger bets would close it faster. The problem is that the deficit has no causal relationship with the probability of the next bet winning. A losing run of ten bets does not change the true probability of the eleventh. Increasing stake size in this context does not increase the chance of recovery; it amplifies variance at the exact moment the bankroll is most depleted and most vulnerable.

Loss chasing is also self-reinforcing when it occasionally works. A bettor who chases a deficit and recovers it has been rewarded for the behaviour, making them more likely to repeat it. The same mechanism that reinforces the gambler’s fallacy also embeds loss chasing as a learned response.

The only structural protection is a pre-set drawdown rule: if the bankroll drops by a defined percentage, stake size is reduced proportionally and no additional bets are placed until the next scheduled review. This rule needs to be written down before the session begins, not invented during it.

The Gambler’s Fallacy: Misreading Randomness

The gambler’s fallacy is the belief that a random independent event is more or less likely to occur based on the outcomes of previous independent events. The classic formulation: a coin that has landed heads five times in a row is “due” to land tails. The probability of tails on the sixth flip is still exactly 50%, identical to what it was before the run began.

In sports betting, the fallacy appears in several forms. A team that has lost its last five matches is assumed to be “due” a win. A tipster who has given ten losing selections in a row is assumed to be “due” a winner. A market that has settled on the underdog for three consecutive weekends is assumed to be “overdue” a favourite. None of these assumptions have any basis in probability.

Psychologists Amos Tversky and Daniel Kahneman traced the fallacy to what they called the representativeness heuristic: the tendency to expect small samples to reflect the statistical properties of large ones. People intuitively expect a short sequence of coin flips to contain roughly equal numbers of heads and tails, even though short sequences are by definition subject to high variance and frequently deviate from expected proportions.

A 2025 study published in Scientific Reports confirmed that the gambler’s fallacy is prevalent even among experienced participants in repeated betting tasks, and found that both the frequency and duration of consecutive outcomes influence the strength of the fallacy. Critically, the research found no reliable way to eliminate the bias through information alone, which reinforces the case for process-based decision rules over in-the-moment judgement.

The correction is to treat every bet as statistically independent of past results. Building your analysis from the true probability of the outcome rather than from the recent sequence of results keeps the focus where it belongs: on the odds and the edge, not on the streak. Understanding how implied probability converts bookmaker prices into percentage chance is the analytical starting point for this kind of independent assessment.

The Hot-Hand Fallacy: The Mirror Image

The hot-hand fallacy is the inverse of the gambler’s fallacy. Where the gambler’s fallacy assumes a streak is “due” to end, the hot-hand fallacy assumes a streak is likely to continue. A team that has won four in a row is perceived as being “on form” in a way that inflates their true probability beyond what the underlying data supports.

In betting markets, this manifests as the public overvaluing recently successful teams and overvaluing tipsters on winning runs. Bookmakers frequently exploit this by leaving odds on in-form teams slightly compressed relative to true probability, knowing that public sentiment will drive further volume. Bettors who monitor opening odds versus closing odds can observe this directly: lines on popular teams in good form often shorten between opening and close purely due to sentiment-driven volume rather than new information.

The correction for both fallacies is the same: anchor probability estimates to large, stable sample sizes rather than recent sequences.

Confirmation Bias: Seeing What You Want to See

Confirmation bias is the tendency to search for, interpret, and weight information in a way that confirms a belief you already hold, while unconsciously filtering out evidence that contradicts it. It is one of the most documented biases in human cognition. In betting, it is particularly destructive because it systematically distorts probability estimation.

A bettor who has decided they want to back a team will, without realising it, give greater weight to statistics that support that view (recent form, head-to-head record in favourable conditions) and less weight to the evidence that challenges it (injury news, a difficult fixture list, defensive weaknesses against the opponent’s tactical setup). The result is a probability estimate skewed in the direction of the bet they wanted to place before the analysis began.

This is the mechanism that turns genuine research into the illusion of research. The bettor has done the work, reviewed the data, considered the context. But the conclusion was decided before the process started.

The structural fix is to assess evidence against a position as deliberately as evidence for it. Before finalising any probability estimate that feeds into a value bet calculation, list the two strongest reasons the bet should not be placed. If those counterarguments cannot be dismissed with specific evidence, the probability estimate needs revision.

Recency Bias and Anchoring: Two Distortions of Context

Recency Bias

Recency bias is the tendency to assign more weight to recent events than older ones when forming expectations about the future. In betting, it typically produces two errors: overvaluing teams or players in strong recent form, and undervaluing those in temporary poor form.

Both create mispricing opportunities when the bookmaker has not corrected for the same bias in the market. A team that has won three in a row attracts heavy public backing, compressing their odds beyond what the underlying probability justifies. The opposing side lengthens in response, often creating value on the side being underrated by the recency-driven public.

The correction is to anchor probability estimates to larger sample sizes. Three to five matches is not a statistically meaningful sample for most football markets. Ten to twenty is more reliable. Performance metrics that are more stable over time (expected goals, defensive shape consistency, head-to-head records in similar conditions) are more informative than raw result sequences.

Anchoring Bias

Anchoring bias is the tendency to over-rely on the first piece of information encountered when forming a judgement. In betting, the most common anchor is the opening price. A bettor who sees a team open at 2.50 will subconsciously treat that number as a reference point when evaluating subsequent prices. If the same team is later available at 2.80, the bettor may perceive this as unusually generous value relative to the anchor, even if their own independent probability estimate would place fair odds closer to 3.00.

The practical consequence is that bettors who look at the odds before forming their own probability estimate are anchoring their analysis to the bookmaker’s view rather than building an independent one. The correct sequence is to estimate true probability first, then compare it against the available price. Forming your estimate before looking at any price is the simplest structural defence against anchoring.

Overconfidence and the Illusion of Control

Overconfidence in betting takes two related forms. The first is overestimating the accuracy of your probability estimates relative to the bookmaker. The second is the illusion of control: the belief that skill, research, or familiarity with a sport gives you significantly more information than the market has already priced in.

Both are natural responses to winning runs. A bettor who hits seven winners from ten selections in a fortnight will often attribute that run primarily to skill rather than variance, and will increase their stake sizes accordingly. When the variance corrects, the increased stakes turn a routine losing period into a meaningful bankroll drawdown.

The research consistently shows that most recreational bettors overestimate their win rates when asked to self-report them. When records are actually kept and reviewed, the picture is usually more modest. Genuine edge in liquid, well-traded markets is small, typically in the range of 3-7% for skilled bettors, and it only emerges reliably over hundreds of bets.

A related manifestation is fan loyalty bias: the tendency to back a team because you support them rather than because the price represents genuine value. Emotional attachment to a team produces probability estimates that are structurally skewed in their favour regardless of the actual evidence, which is confirmation bias operating through identity rather than analysis.

The antidote is compulsory tracking. Recording every bet with the estimated probability before placement and the actual outcome after it forces a continuous comparison between prediction and reality. Over a meaningful sample, the gap between perceived accuracy and actual accuracy becomes visible and actionable. The expected value calculator makes probability estimates explicit at the selection stage, which makes them harder to inflate unconsciously.

The Sunk Cost Fallacy: Throwing Good Money After Bad

The sunk cost fallacy is the tendency to continue a course of action because of previously invested resources rather than because of the future expected value of continuing. In betting, it appears most visibly in the urge to “get back to even” after a losing session, treating the session loss as a debt that needs to be repaid before stopping.

The money already lost in a session is gone regardless of what bets are placed next. The question at any point is purely forward-looking: does this particular bet, assessed independently, have positive expected value at the available odds? If the answer is no, the size of the prior loss is irrelevant to the decision.

The sunk cost fallacy is closely related to loss aversion. Both involve fixation on prior losses. The distinction is that loss aversion drives the emotional response (the pain of the loss), while the sunk cost fallacy drives the rationalisation (the logic that the loss somehow obligates further action).

The practical response is to treat each session as beginning from zero and to evaluate each bet on its own merits regardless of the session’s running total. Some bettors implement a hard stop rule: if a session loss exceeds a defined threshold, for example five units, no further bets are placed that day. This converts a psychological problem into a mechanical rule.

Tilt: When Emotion Takes Over Completely

Tilt is a term borrowed from poker that describes the state of emotionally compromised decision-making that typically follows a significant loss or a sequence of losses. A bettor on tilt abandons their process: they increase stakes, ignore their selection criteria, place bets on markets they do not normally follow, and act in ways that, under calm conditions, they would immediately recognise as irrational.

Tilt is not a character flaw. It is a predictable neurological response to loss under conditions of risk. The same brain systems that process financial losses also process physical pain, and the response to sustained loss can trigger the same fight-or-flight instincts that evolved to respond to immediate physical threat. None of those instincts are useful for making accurate probability assessments.

In-play betting creates a particularly high-risk environment for tilt. The combination of fast-moving odds, real-time emotional stakes, and minimal time for rational assessment removes most of the structural protection that pre-session planning provides. A bettor who would not ordinarily bet on live markets but places an in-play bet mid-session to chase a losing position is exhibiting a classic tilt response accelerated by the format.

The most reliable protection against tilt is to recognise its early warning signals and have a pre-agreed response to each one. Common early signals include the urge to place a bet outside your normal selection criteria, the urge to increase stake size to recover a deficit, a sense of urgency or frustration that was not present at the start of the session, and the feeling that you are “owed” a winner.

The agreed response to any of these signals should be a complete stop: close the bookmaker tab, leave the session, and do not return until the next scheduled review. This preserves capital for the next session, when decisions will be made from a rational state.

Building a Process That Works Against Your Biases

No bettor can eliminate cognitive bias through willpower alone. The biases described in this article are documented features of human decision-making under uncertainty, present across all educational and professional backgrounds. The only reliable counter is a system that reduces the number of in-the-moment decisions where bias can operate.

The five core elements of a bias-resistant betting process are:

Pre-commitment means deciding all selection criteria, stake sizing rules, and stop conditions before looking at any odds. Write the process down rather than holding it in memory, so it cannot be quietly revised mid-session when emotions are elevated.

Process tracking over outcome tracking means recording estimated probability alongside the result of every bet, then reviewing whether your estimates are calibrated over a sample of at least 200 bets rather than reviewing whether the last session was profitable. A well-calibrated bettor who runs badly for two weeks has not changed anything important. A poorly calibrated bettor who runs well for two weeks has not discovered anything real.

Scheduled reviews means reviewing performance monthly, not nightly. Nightly review gives loss aversion and recency bias fresh material to work with after every session. Monthly review forces assessment of the trend rather than the most recent data point.

Deliberate counterargument means listing the two strongest reasons not to place every bet you are inclined to place before finalising the decision. This directly counters confirmation bias by forcing engagement with disconfirming evidence before the stake is committed.

Hard stops means defining the session loss limit, the drawdown trigger for reducing unit size, and the conditions under which no bets are placed (post-tilt, outside scheduled hours, on markets outside defined criteria). These rules need to exist before the conditions that trigger them arrive, not be invented in the moment they are needed.

FAQ

QWhat is the most damaging cognitive bias in sports betting?

QWhy do bettors keep losing even when they know about cognitive biases?

QWhat are the signs of being on tilt?

QWhat is the difference between the gambler's fallacy and the hot-hand fallacy?

QDoes experience reduce cognitive bias in betting?

QHow does betting psychology relate to bankroll management?